The global сircular economy roadmap: trends, barriers and the new “standard of frictionless trade”

The global secondary smartphone market has reached a critical turning point, evolving from a niche “green” initiative into a sophisticated financial instrument for digital affordability. These shifts were the focal point of the Circular Market 2026 conference in London, where industry leaders shared their observations and strategic insights. As noted by Breezy CEO Andrii Kosar…

The global secondary smartphone market has reached a critical turning point, evolving from a niche “green” initiative into a sophisticated financial instrument for digital affordability. These shifts were the focal point of the Circular Market 2026 conference in London, where industry leaders shared their observations and strategic insights. As noted by Breezy CEO Andrii Kosar and Trade-in Product Manager Jan Mazur, who attended the event, the industry is no longer defined by consumer willingness, but by the efficiency of the ecosystem. As markets mature, the focus has shifted toward removing operational “friction” and integrating trade-in as a strategic ESG and financial KPI.

From the consolidated powerhouses of North America to the high-tech repair hubs of India and the government-backed circulation models in China, here is the 2026 global landscape of the circular economy based on the expertise shared at the London summit.

1. North America (USA & Canada): the benchmark of consolidation

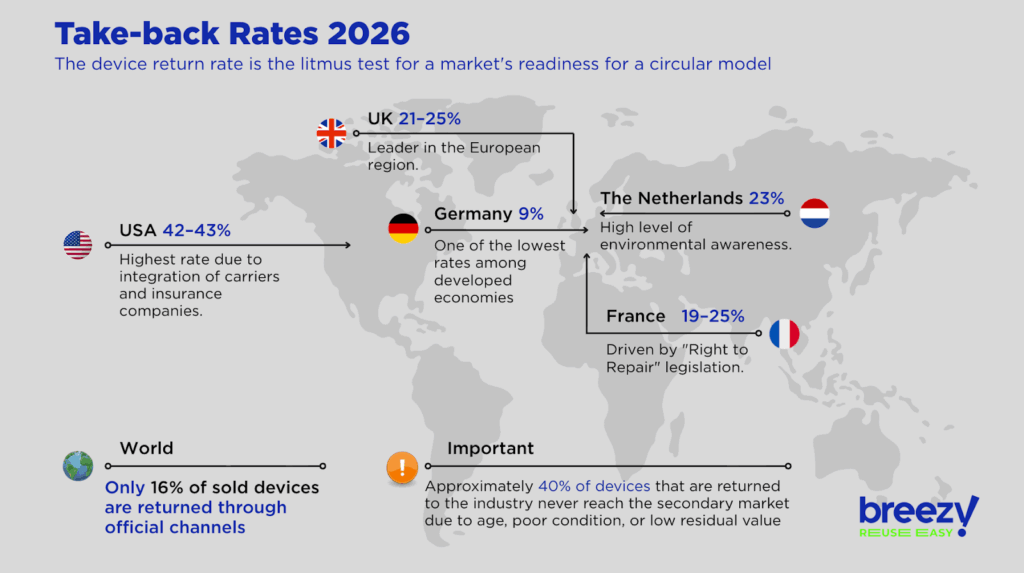

North America remains the global gold standard with a 42–43% Take-back Rate. As Ricardo Chang (Samsung UK & Ireland) noted, such high efficiency is the result of a deeply integrated ecosystem where carriers, insurers, and OEMs collaborate seamlessly to manage device lifecycles. This synergy of Installments + Trade-in—has effectively turned premium flagships into a mass-market standard, turning into the primary driver for lowering entry costs and ensuring device affordability.

Market Dynamics & Strategic Drivers

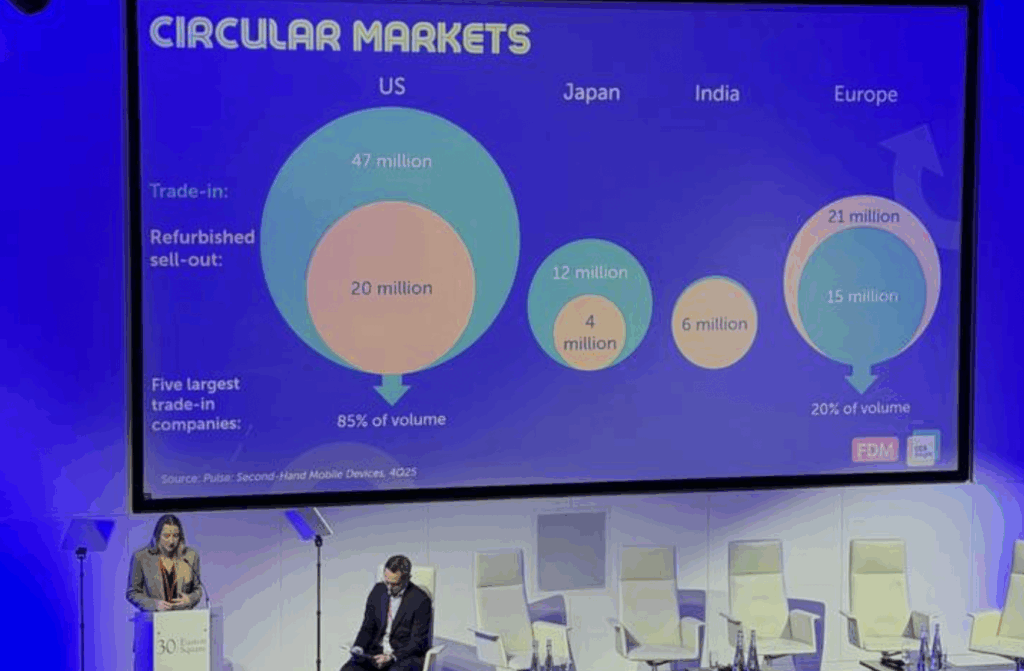

◉ Extreme consolidation (85/5): The region is characterized by intense concentration, where just five players control 85% of the market. This creates massive entry barriers for new competitors compared to the fragmented European landscape.

◉ Global donor: Because of its scale, the US acts as a “net exporter” of high-spec inventory. According to analyst Simon Bryant (FDM | CCS Insight), North America serves as the vital lifeblood for supply-deficient regions like Europe, which struggle with a lack of local high-quality supply.

◉ Shifting retention: A new strategic trend is emerging where carriers increasingly retain collected devices for their own internal refurbished programs to capture more value, rather than offloading them to third-party wholesalers.

Operational Reality & Bottlenecks

◉ Supply leakage: Despite high collection rates, nearly 40% of devices never reach the secondary market. Jessica Miller (FDM | CCS Insight) attributes this “leakage” to extreme obsolescence, poor physical condition, or a residual value so low that repair and processing costs become prohibitive.

◉ Pricing paradox: The market faces a structural contradiction where major networks often offer the lowest buy-back prices, while retailers are forced to heavily subsidize trade-in deals to remain competitive and drive new hardware sales. (by Jessica Miller)

◉ B2B paradox: The enterprise sector shows over 70% return rate through leasing and lifecycle management. However, deep-seated security fears—particularly in the healthcare and finance industries—still frequently lead to the secure disposal of devices instead of their resale. (by Jessica Miller)

ESG & External pressures: Trade-in has officially transitioned into a core ESG KPI. Davide Tacchino (Vodafone) points out that this shift is accelerated by external economic factors; specifically, rising DRAM prices are expected to drive more consumers toward the refurbished segment as new device prices continue to climb.

2. Europe: supply shortage and “contractual” stability

Europe is a high-growth region defined by supply shortages and extreme fragmentation, still trailing the North American “gold standard” in efficiency.

◉ Supply & regulatory barriers: Domestic supply is insufficient, forcing a heavy reliance on imports. Sandeep Shetty confirms that nearly half of Europe’s secondary devices are imported. However, Davide Tacchino (Vodafone) highlights a major bottleneck: many operators reject US/Japan shipments because they lack a physical CE-mark on the chassis, even if digital marking is present.

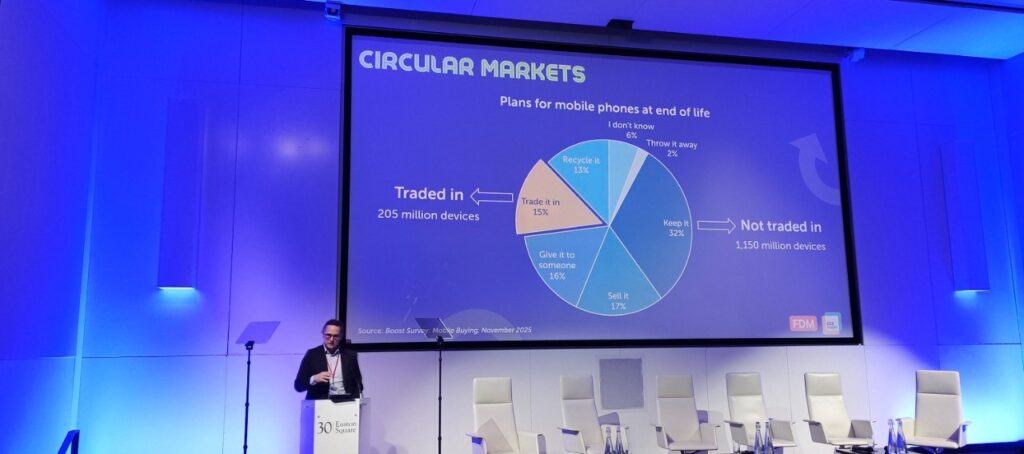

◉ The ecosystem leak (90%): Around 90% of devices “leak” into gray markets or sit in drawers. Ricardo Chang reports an average trade-in rate of just 10% (9% in Germany), while Simon Bryant estimates over 1.2 billion devices are lost annually to the informal sector, driven by data privacy fears and low valuations.

◉ Market fragmentation & grading: Jess Miller points out that Europe’s top five players control only 20% of the market (vs. 85% in the US). Furthermore, Davide Tacchino emphasizes that the lack of unified “A+/B” grading standards creates a “huge headache” for customers and blocks industry growth.

◉ Regional leaders: According to Ricardo Chang, three countries lead the region — UK (21–25%), Netherlands (23%), and France (19%).

*According to data from Jessica Miller (FDM | CCS Insight)

“Why do 60% of phones ‘die’ in drawers? It’s not the people; it’s the friction. By simplifying pricing and logistics, we saw return rates jump to 40%. A user is motivated at $260–$270, but below $75, the device stays home, losing 2% of its value every month. Our goal is to close the gap between the 87% who know about trade-in and the 44% who actually do it,” — said Richard Chang, Head of Samsung UK & Ireland for Mobile Experiences, from the stage of Circular Markets.

3. Africa: A laboratory for accessibility and impact investment

The African continent shows the highest growth rates in the secondary market. Here, a pre-owned smartphone isn’t just “second-hand”—it’s a primary tool for digital inclusion. As discussed during the panel sessions at Circular Market 2026, trade-in (TI) is becoming the “missing link” for telecom operators. Without affordable devices capable of supporting modern networks, massive investments in infrastructure remain underutilized, stalling regional development in areas like distance learning and digital entrepreneurship.

The usage gap & the connectivity barrier. While infrastructure development has moved at a rapid pace, a significant “usage gap” persists across the continent. Davide Tacchino (Vodafone) highlighted a stark reality: although 4G networks cover approximately 70% of the African population, actual usage remains stalled at just 10%.

◉ The price barrier: According to Tacchino, the primary obstacle isn’t the lack of signal, but the prohibitive cost of new hardware.

◉ Internet as a basic good: Since high-speed connectivity is now recognized as an essential public good—vital for education and business—the industry is pivoting toward the secondary market to bridge this gap.

As a key player in this transformation, Breezy provides its services through high-tech partnerships in South Africa, proving that transparency and technology can unlock market potential. These initiatives directly align with the UN’s Sustainable Development Goal 9 by bridging the “digital divide” and expanding universal access to essential information and communication technologies.

◉ End-to-end Trade-in with AI-driven valuation: In partnership with AVO, Breezy provides AI-powered remote evaluation for 3 million customers. This digital-first approach allows for an instant upgrade process, making the transition to a new smartphone seamless.

◉ B2B innovation & logistics: The first in the region door-to-door B2B trade-in model was introduced with Digital Generation. This automated process allows businesses to swap old fleets for new Apple equipment without leaving the office.

◉ In-store Trade-In at scale: Trade-In by Breezy is available across 89 Incredible Connection stores in South Africa. Customers receive instant, competitive pricing powered by automated Apple Diagnostics — now available in Africa through Breezy — alongside AI-based photo evaluation. This combination ensures fast, accurate grading and maximized buy-back value directly at the point of sale, creating a seamless omnichannel experience.

At Breezy, we see immense prospects in Africa. Our presence in South Africa is already a proven launchpad for scaling, and it’s just the beginning of our ambitious expansion into emerging markets. We are here to turn the region’s potential into true digital accessibility

4. China: trade-in as a state program

The recent transformation of the Chinese market was a central theme of the presentation by Jeremy Ji (ATRenew). At the start of 2025, the Chinese central government catalyzed the market by introducing aggressive trade-in promotions.

◉ Direct Discounts: Consumers now enjoy a 15% discount on devices priced under 6,000 RMB (approx. $630).

◉ Government Backing: This isn’t just a store sale; it’s a national strategy to encourage the circulation of new products through accessible trade-in pathways.

China has solved the “trust gap” in the pre-owned market through a mix of human touch and advanced physics.

◉ The Doorstep Exchange: In top-tier cities like Beijing and Shanghai, 90% of transactions happen via a dedicated “two-door” service. A team member delivers your new phone and evaluates your old one on the spot, ensuring a high conversion rate through person-to-person trust.

◉ Precision Diagnostics: they use X-ray scanning to find unauthorized internal parts and computer vision to automatically detect external dents or scratches. This automated QC process flags functional errors instantly, making the inspection almost entirely hands-free.

Perhaps the most significant shift is China’s new role in the global trade cycle.

◉ Strategic Exporting: China is increasingly viewed as an exporting nation for high-quality pre-owned tech rather than an importer.

◉ Setting Global Rules: China is now an active member of ISO organizations (QC245), leading study groups to standardize cross-border transactions for second-hand goods, ensuring these devices find a second life in international markets without impacting new product sales.

5. India: the world’s repair shop

According to Mandeep Manocha (Cashify), India has built a unique, self-sufficient secondary market driven by strict import bans and a lack of operator control. Unlike the US or Japan, brands here had to build their own ecosystems from scratch, leading to a highly efficient, independent landscape.

◉ The “Industry Back-end”: India imports devices exclusively for high-tech refurbishment with 100% subsequent re-export, keeping the domestic and international cycles strictly separated.

◉ The algorithm verdict: A unique psychological shift has occurred where Indian consumers trust machines over humans. If an AI-driven program sets a price of $100, it is accepted as objective truth. While a human’s assessment might be seen as biased or having an “ulterior motive,” the machine’s verdict eliminates negotiation and ensures a frictionless transaction.

◉ The doorstep model: Due to historically low trust in postal services and courier reliability, the “doorstep” model is mission-critical. Verification and the final buyout happen directly at the customer’s home, ensuring immediate payment and peace of mind.

Despite its efficiency, the market faces a significant Credit Gap. While Indian banks and financial institutions aggressively fund the purchase of new gadgets, they remain hesitant to finance or insure the risks associated with used technology.

We don’t just follow trends; we set them on the markets of operations. Our AI-driven evaluation has been successfully powering both in-store and online operations for a long time, allowing us to provide a truly seamless omnichannel experience. By unifying these channels, we ensure that whether a customer starts their journey at home or finishes it in a shop, they receive the same speed, accuracy, and convenience. This synergy of technology and human expertise is what makes our trade-in ecosystem the most reliable choice for partners and customers alike

6. Japan: currency fluctuations and the corporate sector

Japan’s secondary market is defined by a unique carrier-centric distribution model where, as Tsuyoshi Shimizu (WeSellCellular) points out, most consumers return devices every three years, fueling a high trade-in rate of 30–40%.

◉ The supply paradox: While Japan is a massive exporter, the weak Yen has shifted the inventory mix. Since new flagships (like the iPhone 17 Pro) are becoming prohibitively expensive, the surplus consists mainly of slightly older models rather than the latest tech, creating a market that is strong in volume but “generationally lagged” compared to the US.

◉ Robotic precision: Japanese grading standards are among the most rigorous in the world. To maintain this reputation while cutting costs, companies are heavily investing in robotics and automated processing centers to achieve high levels of consistency and accuracy in device evaluation.

Corporate B2B surge: Corporate demand is increasing significantly for enterprise solutions. Major players like GE Healthcare now procure used iPads in batches of 5,000+ units through structured leasing and base programs, as domestic supply struggles to keep pace with professional demand.

From global trends to operational reality

Many of the structural trends discussed across regions — automation, robotics, AI-driven diagnostics, lifecycle integration, instant discount, and enterprise-grade trade-in — are already embedded in Breezy’s operational model.

Breezy operates its own refurbishment facilities in three countries, combining Industry 5.0 principles, automation, and robotics across approximately 3,000 m² of production space. By maintaining unified grading standards and full in-house control over all operations — without relying on subcontractors — we ensure consistent quality at scale. Every refurbished device undergoes standardized multi-stage diagnostics and is backed by a warranty, reinforcing trust and transparency across our ecosystem.

Our trade-in infrastructure supports a broad and diversified intake portfolio of over 10,000 device models — including smartphones, gaming consoles, Apple and Windows laptops, tablets, and wearables — enabling partners to unlock value across multiple product categories rather than relying on a narrow flagship-driven strategy.

In parallel, Breezy places a strong strategic focus on the B2B segment. Our flexible cooperation models and dedicated teams allow enterprises of different sizes to structure device buy-back programs efficiently — making corporate fleet renewal and asset recovery increasingly mainstream across our markets.

Bringing this ecosystem together is Breezy’s multi-buyer pricing platform — a structured bridge between large-scale buyers, retailers, telecom operators, and end users. By naturally balancing supply and demand across the network, the platform enables transparent price formation and helps deliver highly competitive buy-back values while maintaining market sustainability.

Rather than observing global shifts, Breezy is actively operationalizing them — building a scalable, technology-driven secondary ecosystem aligned with the new standard of frictionless trade.

Ready to lead the circular revolution? Don’t let operational friction hold your business back. Contact Breezy today—we’ll help your business launch a seamless, high-tech trade-in ecosystem that turns global trends into your competitive advantage.

What will end the era of greenwashing in tech: insights from MWC 2026 Barcelona

Imagine this: a Fairphone can be disassembled with a screwdriver in minutes and used for 7 years, while Deutsche Telekom shuts down base stations for milliseconds at a time—resulting in lower connectivity costs for customers. The Breezy team, including CEO Andrii Kosar and Trade-in Product Manager Jan Mazur, has returned from MWC 2026 in Barcelona….

The secondary market as the new center of gravity: Insights from Circular Markets London 2026

The secondary mobile device market is no longer a supporting channel — it is becoming a structural driver of revenue, retention, and long-term margin stability across Europe. At Circular Markets London 2026, Breezy CEO Andrii Kosar and Trade-in Product Manager Jan Mazur joined industry leaders to discuss the shifts redefining the market: affordability replacing sustainability…

The future of circular IT: Key insights from Retech Days Business 2025

On November 27, Breezy attended Retech Days Business 2025 — one of the key events in the circular IT and sustainable electronics industry.Our colleague Maria Yanchenko took part in a panel discussion focused on device lifecycle extension, end-of-life management, quality standardization, and building trust in refurbished technology. For those who couldn’t attend, we’ve gathered the…

International

International  Ukraine

Ukraine  Poland

Poland  Georgia

Georgia  Kazakhstan

Kazakhstan  Cyprus

Cyprus  Azerbaijan

Azerbaijan  Moldova

Moldova